EXPERT OBSERVER

Amid the spread of coronavirus, the past few weeks

have seen increased expectations of an Australian recession, a slowdown in

business activity and trillions of dollars wiped off global share markets. It

has many asking what the impact of the coronavirus would be on Australian

residential property.

This note explores fundamentals of housing to better understand outcomes in the

current climate. It is found:

- Housing has performed relatively well against negative economic shocks, but the unique conditions of a pandemic-induced economic slowdown must be considered;

- Housing is an illiquid asset and a consumption good, which shows far less volatility and decline than share markets;

- In the coming weeks, property transactions may fall significantly, but the impact on values is unclear; and,

- Existing economic headwinds, including high household debt, make the property market particularly susceptible to a fall in demand. However, Australia does not have ‘one’ property market, and a decline in demand will be tempered by the composition of the local workforce, and the state of household finances.

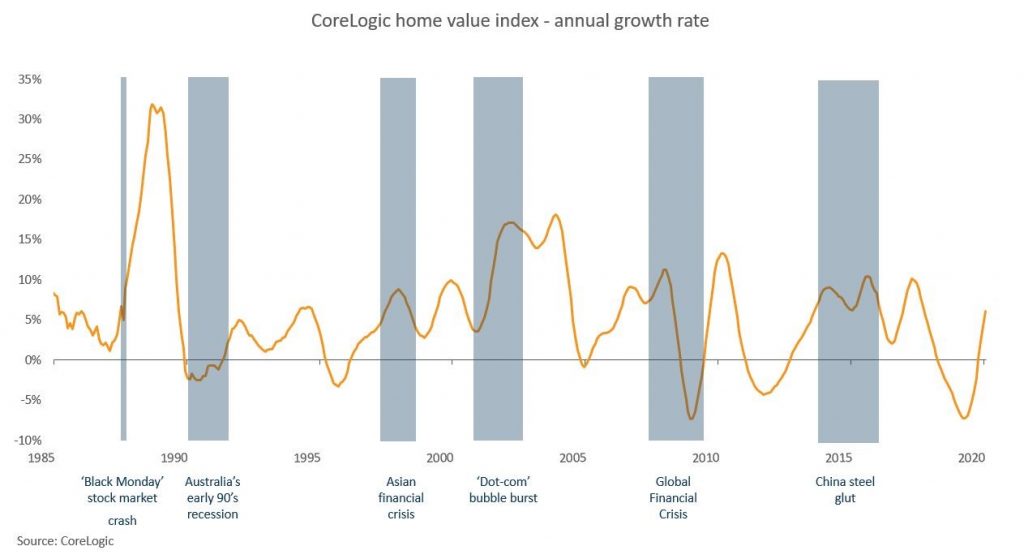

Australian residential property has historically fared well against negative economic shocks

In beginning to assess the impact of the current

slowdown on property, it is worth exploring how property has historically

responded to negative economic shocks.

Major share market losses and recession are not necessarily predictors of

declines in housing values. This can be seen in the figure below. When

significant, negative economic shocks occur, the effect on the housing market

varies. Property value changes depend on the level of impact on Australian

industry.

As an example, the 1987 ‘Black Monday’ stock market crash was a negative shock,

in which the Australian share market lost approximately 23% of its value in a single day.

But housing values were largely unaffected. By October of 1988, residential

property values experienced double-digit growth, as financial deregulation

contributed to asset value inflation.

In the 12 months to January 1988, the Australian unemployment rate declined 60

basis points. The Hawke government also reinstated negative gearing as we know

it today, after temporarily quarantining any losses associated with rental

property between 1985 and 1987. This may have provided an extra boost to

Australian property investment at the time.

By the early 1990’s, Australia experienced a recession and property values

declined, but only by -4.4%, from June 1989 to October 1990.

In 2007-08, when the GFC began, the Australian economy was more globalised. A

slowdown in the global and domestic finance sector affected employment, incomes

and subsequently borrowing capacity for housing.

The national dwelling market declined -7.5% from February 2008 to January 2009.

However, an uplift in mining-related investment, the start of a rate cutting

cycle and government stimulus saw a fairly swift recovery.

Recently, values been more reactive to structural changes in the lending space.

Between 2014 and 2017, a series of policies limiting investment housing lending

catalysed one of the largest and longest property market downturns since the

early 1980’s. However, further rate cuts and eased serviceability assessment

prompted an owner-occupier led rebound.

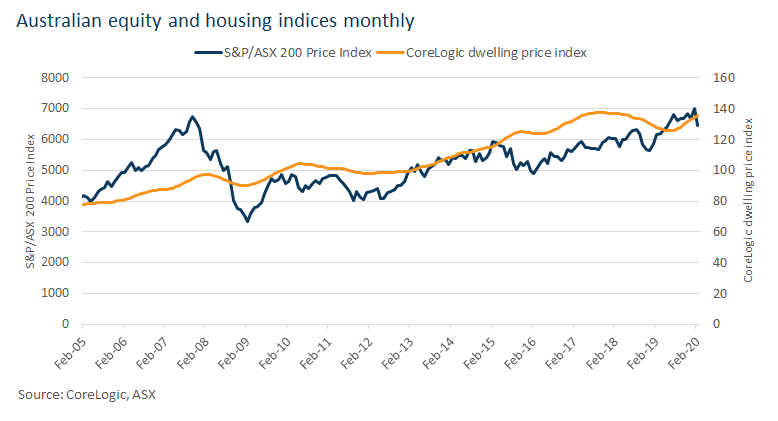

The share market and housing market perform differently

Aggregate figures on the housing market suggest that the slowdown in economic activity from the coronavirus has not impacted housing markets in the same way as equities. This is nothing new. Historically, comparing the S&P ASX 200 index with the CoreLogic home value index, suggests that property responds to macroeconomic conditions at a lag, and avoids the same extent of decline or volatility.

There are a couple of reasons for this:

- The relative illiquidity of housing (high transactional costs and long settlement periods) means it takes longer for property to transact, which makes ‘flights to’ or ‘sell-offs’ of property less likely amid economic uncertainty; and,

- Housing is used as a

consumption good, and is less likely to be speculated upon relative to

equities.

The latter point is a particularly insulating factor at the moment. Since the start of the property market upswing in June 2019, investors comprised 28.2% of the new finance taken out to buy property. This is down from 39.5% in the previous upswing.

In other words, the retreat of investors from

residential property will not have as large an impact as it would have two

years ago.

The relatively low levels of foreign interest in the Australian dwelling market

over 2019 also means there is less risk to the market from declines in this

buyer group. According to the latest NAB residential property survey, foreign buyers in the December quarter of 2019

made up 7.0% of new property purchases (down from the survey average of 10.2%),

and 3.8% of established property (down from the survey average of 6.1%).

Some will be exposed to a downturn in international market participants from

travel bans. These include new unit projects targeting foreign buyers, and

landlords who are reliant on foreign students or tourists for rental occupancy.

Property is not completely insulated from economic events. Depending on the

extent of spread of coronavirus and institutional responses, reduced business

activity could materially slow the flow of income and credit. This would have

significant impacts for the property market.

Sales activity likely to decline, while the impact on values is less clear

Property transaction volumes are likely to fall in

the coming months, but the outcome for values depends on temporal expectations

around coronavirus, and longer-term employment conditions.

In the short term, the coronavirus and subsequent share market declines have

already had a significant impact on consumer confidence. This may lead to postponed

dwelling purchases, as housing is an expensive, high commitment purchase

decision.

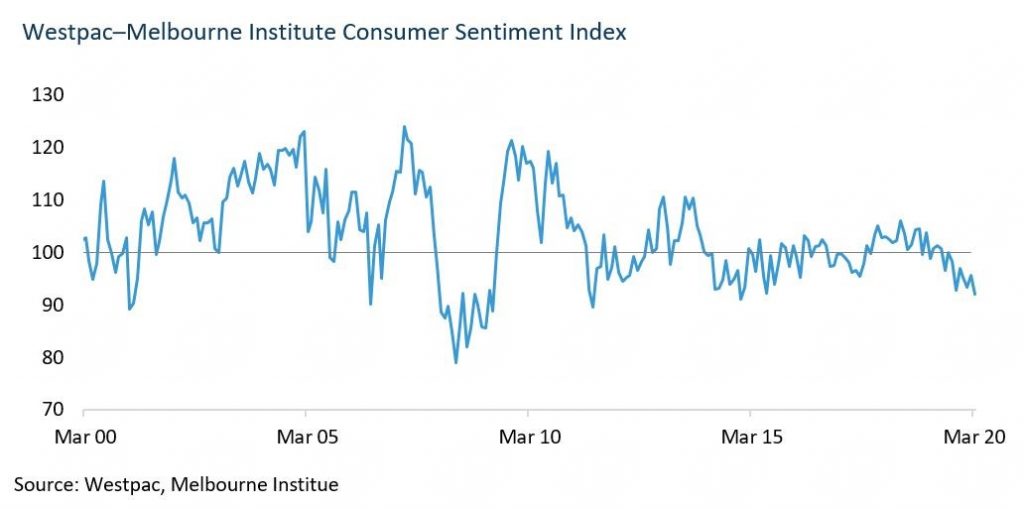

The Westpac-Melbourne Institute Consumer Sentiment Index declined -3.8% over

March to a 5 year low, and recorded the second lowest reading since the GFC.

The index is still 15.3% higher than the level at which it bottomed out in

2008, suggesting consumers are less worried about the economy than at the GFC.

Interestingly, the ‘time to buy a dwelling’ index component only fell -0.3% in

March, but declines may soon deepen. The ‘house price expectations’ sub index

fell more sharply, down 6.6% in March. This was the largest fall since February

last year.

A more direct impact on transactions could be the rise of isolation

precautions. If Australian governments follow quarantine measures enforced

in Italy and China, then inter-city travel would be restricted, and

confinement to the home would prevent physical inspections and on-site

auctions.

While this may seem extreme, it is not unlikely: Victoria and the ACT have

declared a state of emergency across the regions, increasing power of health

ministers to enforce self-isolation.

This presents a challenge to the real estate sector, which often necessitates

physical inspection of property and, in the case of auctions, bidding

environments involving groups of people.

Real estate industry professionals may respond by offering private inspections

rather than open homes, virtual inspections using technology, or remote

auctions. But such technologies can be difficult to adopt in the best economic

conditions. Prospective buyers and sellers are likely to postpone activity

until conditions revert to normal.

Property values may not be impacted the same way.

One important facet of the unfolding economic slowdown, is that it is led by

institutional responses to the coronavirus pandemic. This is a unique cause for

halting production and consumption.

Vendors may view the current pandemic as a temporary economic condition. If

monetary and fiscal stimulus can adequately support business and household

income amid the slowdown, then the next few months could see a sharp

contraction in sales volumes, but not necessarily dwelling values.

This is because the expectation would be for market activities to return.

Influenza periods for example, typically last 3-4 months. It is unclear whether

coronavirus will be seasonal, but, after mass quarantines, China is now showing

a slowed spread of the coronavirus. South Korea is also seeing a drop off in new reported cases after a

social distancing campaign.

A comparison may be drawn with the high seasonality in sales volumes usually

seen around annual holiday periods. Over the past two decades, the decline in

sales volume activity from the month of November to December averaged -15.9%,

and sales volumes in December have a seasonal factor of 0.9. By comparison, the

past two decades have seen an average 0.2% uplift in values from November to

December, with very little seasonality present.

While the current pandemic is by no means a holiday, it is temporary. Unless

the current slowdown presents a significant drag on incomes, vendors may not

see the need to lower their property value expectations.

Headwinds for housing demand

In the long term, housing market values and

activity will be linked to the extent that quarantine measures affect income,

employment, borrowing capacity and credit availability.

The largest and most direct industry shocks from the coronavirus are expected

in:

- tourism, where increasingly strict quarantine procedures deter travel;

- education, due to fewer foreign students being able to travel;

- hospitality, where social distancing leads to a decline in café, bar and restaurant visitation;

- retail, which will be dragged down by low consumer confidence levels; and,

- arts and recreation, where

visitation to theatres , cinemas and art galleries are already on the

decline.

GDP growth in the March quarter was initially expected to be about 50 basis points

lower from what it otherwise would have been. But research on the impact of past influenza

pandemics suggests the losses may be greater.

Unlike the global financial crisis, where a mining boom, as well as monetary

and fiscal policy were effective in helping Australia avoid recession, the

domestic economy now faces new challenges:

- Australia is not expecting

another mining boom. GDP figures for December show that mining investment

is 19.7% lower than where it was at December 2008.

However, the RBA are confident in an uplift in the sector over the year, and note that commodity prices have been fairly resilient amid share market declines.

- There is ongoing weakness in

the private sector. Annual changes in private sector spending have been

negative since June 2019. This has knock-on effects for employment and

income growth, which in turn limits borrowing capacity for property.

The recently announced stimulus package handed down by the Morrison government goes a long way in targeting businesses investment, with up to $25,000 available for small to medium enterprises, apprenticeship wage subsidies and an increase in the value threshold for instant asset write offs to $150,000.

- There is less room to reduce

the cash rate. During the GFC, the RBA implemented 6 rate cuts, taking the

official cash rate from 7.25% in August 2008 to 3% by April 2019.

Currently, the cash rate is a record low 0.5%. Market expectations currently indicate with certainty that there will be a 25 basis point cash rate reduction in April.

There is not much ammunition left in monetary response, apart from pursuing a quantitative easing strategy. The RBA has indicated they will commence bond purchases and repurchasing operations, which involve on selling government bonds to investors before buying them back at a higher price.

- HOUSEHOLD

DEBT IS NEAR RECORD HIGHS.

Household debt is closely monitored by regulators. September quarter data suggests that both

total household debt to income, and housing debt to income, are just below

the record highs in the June quarter.

At September 2019, total debt to household income was 186.5%. This was mostly comprised of housing debt to income (141.3%). The loss of jobs amid a business slowdown could increase the incidence of non-performing loans, especially since the latest APRA data suggests that an increasing portion of finance (38.6%) is being lent with a loan-to-value ratio of over 80%.

Given the high levels of housing debt in Australia, it is important to consider the risk of increased non-performing loans in the current environment. RBA research suggests that at December 2017, about one third of owner occupier loans had at least a two year buffer in mortgage repayments. However, around one quarter had less than one month’s buffer.

If social distancing measures are in place for an extended period of time, those more vulnerable households at risk of mortgage stress could require targeted intervention to avoid delinquency.

Despite these fragilities, and a technical recession increasingly likely, there are some safeguards that will lessen the blow of a halt in income and employment, and the availability of credit.

Just days after announcing its $17.6 billion

stimulus package, the government is considering a second stimulus package.

On Monday the 16th, the council of financial regulators announced further

supportive measures for credit availability, including the RBA preparing the

start of quantitative easing, and APRA have announced the potential easing of

regulatory requirements to support the flow of credit.

In an address on the 11th of March, the RBA was keen to emphasise that the

virus is ultimately a temporary disruptor to business activity, and that eased

monetary conditions and fiscal policy would help the economy to “bounce back quickly once the virus is

contained”.

Not all markets will be equally impacted

Importantly, Australia does not have ‘one’ housing market. While this note considers the residential market in aggregate for simplicity, economic downturns have certainly created more acute, localised declines in property, such as;

- The collapse of mining related infrastructure projects in 2014, which still see Darwin property values more than 30% below the record high;

- Over-supply in the Brisbane unit market, where the latest data shows values are still -11.2% below the record high; and,

- The impact of extreme

weather, storms and flooding, which has suppressed property price growth

in far north Queensland.

Given the idiosyncrasies of the current downturn,

there are likely to be parts of Australia where housing demand, including

rental demand, will fall more sharply than others.

These include areas where workers cannot perform their jobs remotely, and may

have to sacrifice income if social distancing is enforced, where there is a

high incidence of casual employment, and where there is a high concentration of

employment in affected industries.

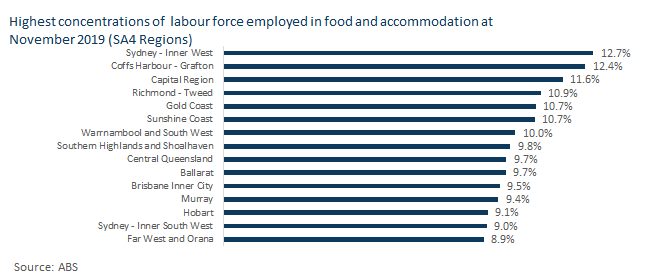

Looking at the concentration of the workforce in accommodation and food

services for example, points to pressure on households in Sydney’s Inner West,

which has the highest portion of workers employed in this sector by SA4 region

(12.7% at November 2019).

Conclusion

The coronavirus outbreak clearly presents some

downside risk for the Australian housing market, but ultimately, the impact

remains highly uncertain. New information and policy responses are unfolding daily,

making it impossible to provide a reasonable forecast of capital growth. Some

added context however, is remembering the fundamentals of the property market,

and idiosyncrasies of a pandemic-led downturn.

Property is less volatile and slower to respond to market shocks than equities,

it is a consumption good and it is tied to fundamentals of employment

opportunity and income growth. In the current climate, the Australian housing

market is more insulated from foreign demand and investment speculation than it

has been over previous years.

Transaction activity is likely to be impacted more than market values. As

consumer confidence reduces, and labour markets are disrupted, more Australians

are likely to put high commitment decisions on hold until there is more

certainty around the economy, jobs and household finances.

Additionally, stimulus measures including emergency level monetary policy

settings and a surge in fiscal spending should help to cushion the impact of

reduced business activity, but a recession in the first half of 2020 still

looks likely.

The current high level of household debt amplifies the risk of unemployment on

housing market conditions. However, areas severely impacted by social

distancing would be less resilient than others in rebounding from the

coronavirus pandemic.

Our views and research on the market outcomes in relation to the coronavirus

will continue to evolve as more information comes to light.

Eliza Owen is the head of Australia research at CoreLogic.

Related Posts

COVID 19 – Public announcement

With the outbreak of COVID-19 (Coronavirus) we want to reassure customers that PROPLAND continues to provide

More than 25% of new Brisbane CBD apartments remain unsold

There’s a black hole in the Brisbane property market. The Inner Brisbane apartment market has